[ad_1]

Of all the tertiary sectors in an economy, logistics is one of the most significant. With the market share of organised players just in single-digits, formalisation of economy along with the ever-so-lucrative and growing retail e-commerce space in India were expected to spur demand for integrated third-party logistics (3PL). 3PL players are those who manage their customer’s supply chain management including logistics, inventory management, warehousing and order fulfilment.

And Delhivery, India’s prominent player in this industry, was in the spotlight recently after signing a definitive agreement to acquire a controlling stake (99.4 per cent) in Ecom Express.

The Ecom Express story

Ecom Express is a pure-play B2C e-commerce logistics player focused on express delivery, a niche within 3PL. Incorporated in 2012, the company even geared up for an IPO and filed its DRHP in August 2024, aimed at raising ₹2,600 crore.

The company’s top five customers which included the likes of Meesho, Amazon and Nykaa among others, contributed 75 per cent of FY24 revenue. Moreover, the top customer group (undisclosed, but widely quoted as Meesho) contributed a staggering 52 per cent, which is a clear case of customer concentration risk.

While such high customer concentration is a clear red flag, read along with the period of association with the customer and the customised offerings presented, the risk might sometimes stand diluted. But in this case, the risk took shape and made a dent.

The phenomenon of captive logistics

Meesho and Amazon, Ecom’s two significant customers, started increasingly insourcing logistics operations in India, the phenomenon being termed ‘captive logistics’. Meesho, through its in-house logistics platform Valmo, started aggregating logistic partners directly from February 2024, thereby reducing reliance on third-party logistics. Amazon India, on the other hand, launched Amazon Shipping and Amazon Freight in December 2024, which while handling its own logistic needs, also offers services to third-party businesses.

As per RedSeer analysis found in Ecom’s DRHP, within B2C e-commerce shipments, while the last-mile shipment volumes rose at a CAGR of 33 per cent during FY20-24, 3PL’s share in it rose from 42 per cent in FY20 to 50 per cent in FY22, before tracing back to 44 per cent in FY24, thanks to the resurgence in captive logistics from FY24, corroborating with the case of Meesho and Amazon India.

A slowdown in business volumes, after a healthy 17.5 per cent CAGR growth during FY22-24, meant that Ecom Express’s revenue stood at ₹1,912 crore for 9M FY25 against ₹2,609 crore for FY24, down 2 per cent (on annualised basis). Net loss, too, after improving to ₹249 crore in FY24 from ₹360 crore in FY23, deteriorated in 9M FY25 to ₹398 crore.

Delhivery’s gain?

From a peak valuation of around ₹7,000 crore in July 2024, Ecom Express is now being acquired by Delhivery for ₹1,407 crore (0.54 times Ecom’s FY24 revenue), 80 per cent down in just nine months.

The important question now: How does Delhivery gain from this acquisition?

As was the case with Ecom Express, Delhivery’s volume growth from the express delivery segment has slowed down in 9M FY25 to a mere 1.8 per cent, after a 36.8 per cent CAGR growth during FY21-24. With this acquisition, Delhivery has bought out its closest competitor in the segment and can consolidate market share by building scale with the existing infrastructure of both the entities.

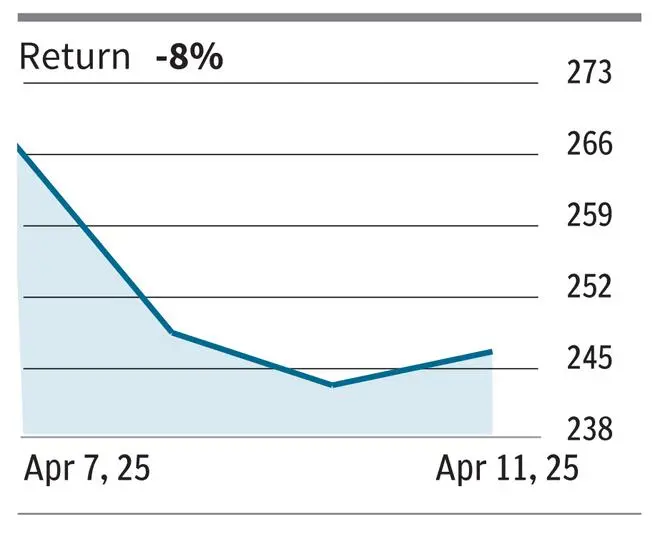

Delhivery closed trading on Friday at ₹246.85 per share, shedding 8 per cent during the week. But with almost 100 per cent overlap of customers between the two entities, integration is not expected to be complicated. However, investors might be concerned with Delhivery increasing exposure to a segment facing challenges. While the captive logistics phenomenon, an industry-wide headwind, will impact Delhivery’s volumes, the company is relatively diversified, with revenue contribution from express delivery segment brought down from 69 per cent in FY21 to 62 per cent in FY24.

Being the largest player in the industry by a good margin, its comfortable net debt to equity ratio of 0.01 (as of Q2 FY25) and the company turning PAT positive for the first time ever in 9M FY25, are green shoots.

The third-party logistics space might see more action if market conditions remain tough. But as of now, this is the second distress sale in 30 months and one of the biggest acquisitions the industry has seen.

Published on April 12, 2025

[ad_2]

Source link