[ad_1]

Sovereign Gold Bond (SGB) series that were issued five years ago have delivered returns exceeding 100 per cent for investors. The eight matured SGB series completed their eight-year terms recently, with XIRR returns ranging between 13 per cent and 18 per cent (with interest payments). Investors who chose early exit through the RBI’s premature redemption window were also well rewarded. An analysis of the five most recent series offering premature redemption shows XIRR returns of 17-19 per cent.

With gold outperforming in the last five years, SGB series eligible for premature redemption are poised to give attractive returns for investors choosing to exit early currently.

How to redeem

SGBs are gold-backed securities issued by the RBI on behalf of the government. Launched in November 2015, SGBs have been issued in 67 tranches. They mature in eight years with a five-year lock-in. Though listed on stock exchanges, trading is limited. However, the RBI offers buyback options at the end of the fifth, sixth and seventh years.

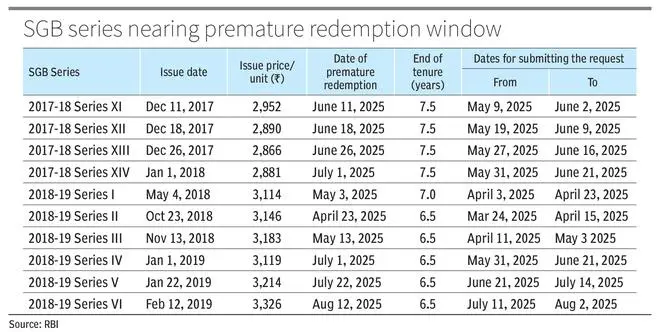

Out of the 59 existing series, 49 have completed five years and are eligible for premature redemption during designated periods. So far, the RBI has facilitated 131 instances of premature redemptions across various SGB series.

Investors can submit premature redemption requests via receiving offices, NSDL, CDSL or RBI Retail Direct during designated periods. Premature redemption requests are accepted from one month before the coupon payout date. The RBI announces a premature redemption calendar biannually, in February and September, listing eligible series for the next six months. To accelerate redemptions, the RBI has now extended flexibility, allowing early exits not just at years 5, 6 or 7, but also at 5.5, 6.5 and 7.5 years. Investors must stay alert to RBI announcements for timely redemption opportunities.

The redemption price will be a simple average of the closing price of gold during the previous week (Monday to Friday), as published by the India Bullion and Jewellers Association. Investors should closely monitor the premature redemption price announced by the RBI, as it is determined based on prevailing gold prices at the time of redemption, which may fluctuate—resulting in a higher or lower payout. The redemption proceeds are transferred to your bank account.

SGBs offer distinct advantages over other forms of gold investment, such as gold exchange-traded funds (ETFs) and physical gold. One key benefit is the fixed annual interest they provide, typically ranging from 2.5 to 2.75 per cent, which other gold options do not offer.

SGBs are more tax-efficient when held until maturity or redeemed through RBI’s early redemption window, as investors are exempt from capital gains tax in these routes. However, if the bonds are sold through the stock exchange, capital gains tax will apply. Interest income from SGBs is fully taxable at your applicable income tax slab rate.

Should you use the premature window?

Unless you face urgent cash needs, holding SGBs until maturity remains a good approach. Gold serves as a hedge against inflation and economic uncertainty. Ideally, gold should comprise 10-15 per cent of your investment portfolio.

If your SGB holdings now exceed your target gold allocation percentage, you can take some profits off the table. In all other cases, staying invested makes more sense—especially as no fresh SGB issues are available—making existing bonds more valuable due to their interest payments and tax-free maturity benefits.

Gold ETFs offer an alternative digital avenue to own gold. However, ETFs lack the interest income and tax benefits of SGBs, and they also charge expense ratios of 0.5-1 per cent, which erode returns over time.

Published on May 24, 2025

[ad_2]

Source link