Lord Kuber was originally considered the guardian of treasures, the king of Yakshas and a protector of wealth. His city, Alakapuri, was said to be filled with unimaginable riches. Despite being the God of wealth, Kuber gradually lost prominence in Hindu traditions compared to Goddess Lakshmi, the Goddess of prosperity. His wealth was often seen as static or hoarded, unlike Lakshmi’s dynamic and flowing prosperity. Additionally, he was frequently depicted as being outshone or even robbed by other figures like Ravana (who is said to have forcefully taken his pushpaka vimana).

Is something similar happening in India’s FMCG sector? Traditionally seen as a safe haven and ‘guardian’ of wealth during turbulent times, the FMCG sector this time around has been punished severely. Consider this: The BSE FMCG index is down 20 per cent since its peak of September 2024 till March 20, as against BSE 500 (-14 per cent) and BSE Midcap (-17 per cent).

Quick commerce impact?

Demand slowdown and persistently-high food inflation were attributed as reasons for the fall. However, we believe, the larger reason is the disruption happening in the distribution segment of the sector led by quick commerce. The promise of delivery within 10 minutes has reshaped shopping habits, reducing visits to traditional kirana stores and even modern trade outlets.

This shift is affecting the FMCG ecosystem. Distributors and dealers, long considered the backbone of the industry, are losing ground to quick commerce players. A clear sign of this trend is the record demand for quick commerce firms during the New Year’s Eve. Blinkit recorded its highest-ever orders in a day, highest orders per minute (OPM) and per hour (OPH), as well as highest total tips given to delivery partners in a day.

Rethinking strategies

The rise of quick commerce has pushed FMCG companies to rethink their distribution strategies. Earlier, general trade (GT) stockists supplied to modern trade (MT) outlets and quick commerce platforms. Now, major FMCG players have set up dedicated teams to supply directly to quick commerce warehouses.

FMCG companies send products directly to quick commerce warehouses, which then supply to the “dark stores” (small fulfilment centres) for final delivery to consumers. This direct approach has boosted margins by 100-200 basis points, making quick commerce an attractive channel.

Hindustan Unilever Ltd (HUL) has taken an even bolder step. It recently announced a new model for major cities, where it will supply products directly to kirana stores. Under this system, distributors will only handle orders and payments, while HUL will manage warehousing and delivery logistics.

Direct dispatch

Unilever PLC (the UK), a global FMCG giant, is increasingly adopting “direct dispatch”, a logistics practice where items are distributed directly from the factory to customers, bypassing intermediaries. The shift is evident in the numbers: In 2018, only 8 per cent of its deliveries used this method; by 2023, this doubled, with a target to exceed 25 per cent by 2026 (Source: Unilever Plc website).

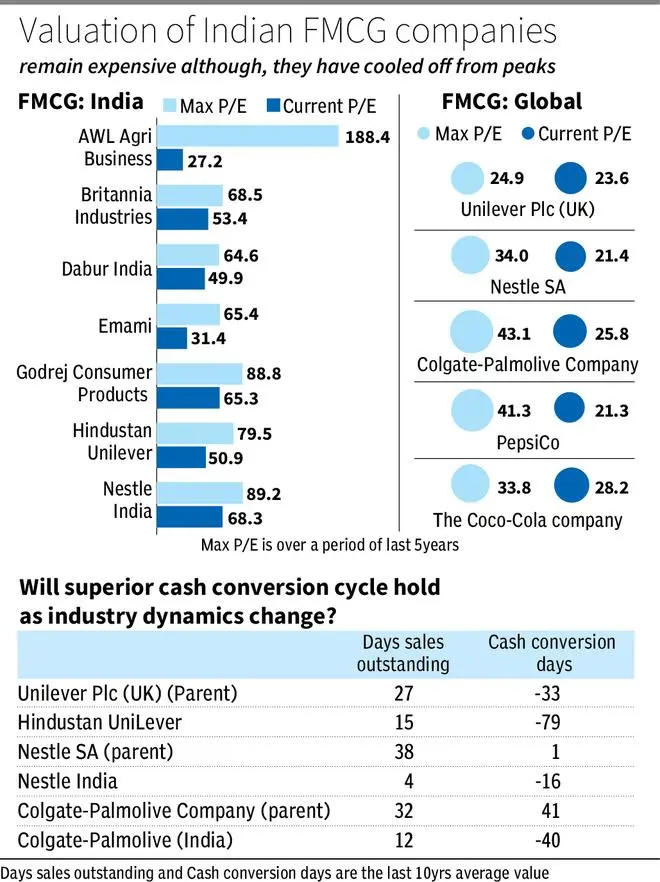

While this strategy aligns well with the quick commerce trend, it comes with a trade-off. As the bargaining power shifts from a fragmented distributor network to a more concentrated model, Indian FMCG companies could face a bloated working capital cycle. Currently, their superior cash conversion cycle is a competitive advantage; however, higher credit demands from quick commerce and increased inventory levels could erode this edge.

Sustaining margins

Quick commerce is a booming $6-billion market, but competition is heating up. Players such as DMart Ready, Flipkart Minutes, BigBasket’s BB Now and Amazon Tez are scaling rapidly. Even Reliance Retail is pivoting towards this model.

This surge in competition is fuelling price wars, leading to massive cash burn across the sector. As the dust settles, industry consolidation is inevitable, leaving only a few dominant quick commerce players in control.

By then, the landscape of FMCG distribution will look very different. India’s one-lakh-plus distributors could shrink in number as the focus shifts to quick commerce. However, the higher margins FMCG companies currently enjoy from this channel are also likely to erode under competitive pressure from peers and new-age direct to customer firms.

Quick commerce has also levelled the playing field, giving emerging brands easier access to consumers. With more players vying for attention, FMCG giants may need to spend more on advertising to maintain brand visibility.

The rise of quick commerce is a double-edged sword for FMCG companies. While it offers an efficient and profitable distribution model today, its long-term sustainability remains uncertain. Price wars, consolidation and changing power dynamics will redefine the sector in the years to come.

Valuations at risk?

The Nifty FMCG Index trades at a steep price-to-earnings (P/E) ratio of 42.4x, making it one of the most expensive sectors in the market. These valuations have historically been supported by the sector’s robust cash-flow management and efficient working capital cycles. Given the underperformance, the weight of FMCG stocks in Nifty 50 index has shrunk from a peak of 11.2 per cent in 2019 to just 7.6 per cent today.

However, quick commerce’s rapid rise is disrupting traditional distribution channels. Margins and receivable days, which have been key pillars of the sector’s valuation premium, are now under threat. Intensifying competition and the need for cost efficiencies could challenge the sustainability of these lofty multiples.

Although the sector has already corrected from its highs, concerns about further P/E contraction remain. Are these valuations a reflection of resilience or a signal of unsustainability in a changing retail environment? Kuber’s stagnancy or Lakshmi’s flowing prosperity? Time will answer.

KR Senthilnathan has contributed to the article. The authors are part of the research team at NAFA Asset Managers