Cipla is facing moderate headwinds at the moment. India business underwent a soft two quarters, US business faced supply issues in one main product and Trump tariff pressure has impacted the sector and Cipla. The stock has corrected 10 per cent from its peak in October 2024. But with an eye on long-term resilience and reasonable valuation at 23.5 times one-year forward earnings, we recommend investors accumulate the stock.

The company has a robust stable of products for the US and is on a strong footing in its branded business to deliver healthy earnings growth. It also has an option to address Trump tariffs with its US plant, if the need arises.

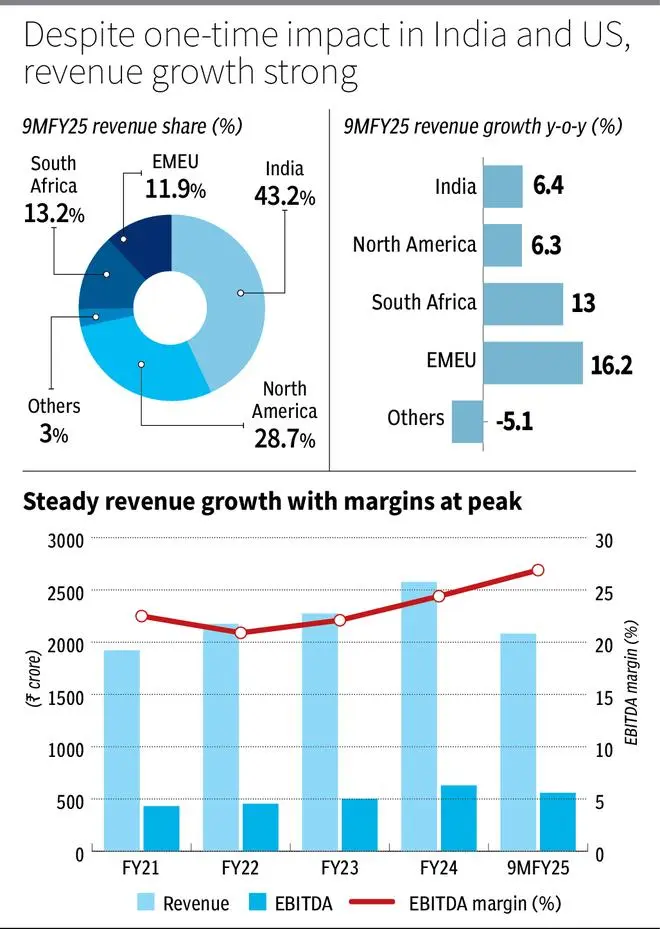

Growth drivers

Cipla has a mostly branded generics business in India and Africa, and a generic and branded business in emerging markets and Europe (EMEU) regions, with a strong outlook.

India business reported a moderate growth of 6 per cent year on year in 9MFY25, as the trade generics channel underwent a distribution restructuring. This exercise is completed, and the sector is expected to return to growth. The acute portfolio serving seasonal conditions was also weak for the year that passed by. The company has a strong branded presence in respiratory and urology, which should sustain growth from pricing and new product introduction along with returning volumes. Cipla is also gearing up for a strong showing in generic – Semaglutide (a GLP-1 product for diabetes) with market formation post India patent expiry next year.

Africa operations are being consolidated under a ‘One Africa’ strategy, which is at least a name-wise replication of the successful ‘One India’ strategy. In India, trade generics, consumer health and prescription have been carved out with leadership, assets and sales force for optimum profitability. African operations, covering 20-plus Capitals and South Africa regions, and a tender business are being reorganised similarly. The region reported 13 per cent year-on-year growth and can continue the momentum with new product launches and margin-focussed operations, especially on the tender side.

The EMEU market has posted a strong sales growth of 16 per cent year on year in 9MFY25. The company is seeking higher penetration in existing markets, new product launches and adding Chinese markets with an operational plant to supplement the region.

US generics

Cipla received clearance (Voluntary Action Indicated) for its Goa plant in October 2024, with the Indore plant being the only one in observation. This has allowed gAdvair and gAbraxane, two coveted generic opportunities into visible range for Cipla.

In the next two years, Cipla should target to launch two products, three peptides and two respiratory products. This should cover the loss of sales in gRevlimid after 2026 and sustain modest sales growth. gAdvair is expected to be launched in H1FY26 and can be a sizeable opportunity with estimated sales of more than $50 million per year. The complicated product can also have a long runway, with Cipla dedicating nearly half a decade for approval and not many competitors on the horizon yet.

The current portfolio is supporting US sales of $230-250 million per quarter. Cipla’s portfolio is largely differentiated with lower contribution from plain generics. This currently includes two respiratory and two peptides. The pipeline should help deliver a similar proportion as well, sustaining US growth for the company.

Financials, valuation

Cipla reported EBITDA margin of 28 per cent in Q3FY25, which is high compared with the 24-25 per cent guidance for FY25. This is on account of a favourable product mix and is likely to taper off. But the company has elevated its margin profile in the last three years (see graph).

With lower plant remediation expenses, moderated R&D expense, lower raw material costs from APIs and improved product mix in the US, India, Africa and EMEU individually, Cipla’s margin profile should stay elevated.

The US tariff imposition will impact formulation makers, but Cipla has US-based plants and if the economics force a change, Cipla is comparatively better placed to come out on top by shifting key products to the US plants.

On the valuation front, Cipla is trading at 23.5 times one-year forward, which is closer to its five- or 10-year average. With the company on a strong footing in all segments, investors can accumulate the stock at these levels for a healthy earnings growth.